Briefing 51

Local Government Financial

Statistics 2000-2001

The Local Government Finance Statistics branch

of the Scottish Executive have recently published the Scottish Local

Government Financial Statistics for 2000-2001.

This publication gives information on local government

finance in Scotland as well as providing information on the income

and expenditure of police and fire services for the year 2000-2001.

The figures in the publication are broken down

to show both capital and revenue accounts and also the split between

the different service accounts operated by local authorities.

The figures on Local Authority accounts within the publication

are split into three broad sections these are Income and Expenditure,

Outstanding Debt and Local Taxes.

Section 1 – Income and Expenditure

Scottish LA accounts have two distinct constituent parts,

the Revenue Account and the Capital Account.

- Revenue Expenditure covers the cost of maintaining local

services and includes costs such as employee salaries and service

operating costs.

- Revenue Income comes from a variety of sources including

Government Grants, local taxes, sales, fees and charges on local

authority services.

- Capital Expenditure relates to the provision and improvement

of tangible fixed assets such as schools, new houses and machinery

that continue to be of value long after their acquisition.

- Capital Income is made up mostly from the sale of these assets.

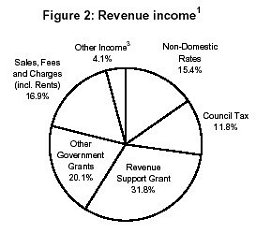

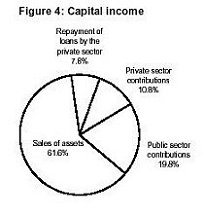

Income

Scottish Local Authority gross income in 2000-01

was £13 billion. This can be split into gross revenue income of

£12.8 billion and also gross Capital income of £0.2 billion, coming

mostly from the sale of fixed assets. Revenue income excluding

special, common good and superannuation funds was £10.9 billion

in 2000-01. Of this, £5.6 billion came from government grants;

£1.8 billion from fees and charges, £1.7 billion from non-domestic

rates and £1.3 billion from council tax. For percentage breakdowns

of LA income from 2000-2001 see Figs 2 and 4 below

Source: Scottish Local

Government Financial Statistics for 2000-2001.

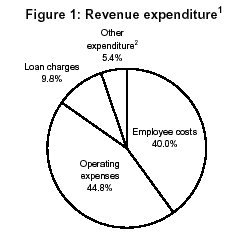

Expenditure

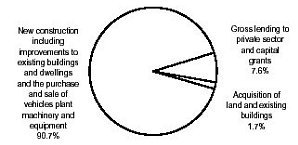

In 2000-01, Scottish Local Authority gross expenditure

was £12.8 billion. This was split into gross revenue expenditure

of £12 billion, and gross capital expenditure on land, buildings

and other major assets of £0.8 billion. Revenue expenditure on

general fund services, housing and trading services i.e. excluding

special, common good and superannuation funds was £11 billion.

Just under half of this £11 billion local authority revenue expenditure

went on education (£3 billion) and housing services (£2.3 billion)

in 2000-01. A further £1.6 billion went on social work services,

with revenue expenditure on law, order and protective services

amounting to almost £1.1 billion. Approximately 40 per cent of

local authority revenue expenditure on general fund, housing and

trading services was accounted for by employee costs with 45 per

cent on operating costs and a further 10 per cent on loan charges.

For percentage breakdown of LA expenditure for 2000-2001 see figs

1 and 3 below

Figure 3: Capital expenditure

Source: Scottish Local

Government Financial Statistics for 2000-2001

Section 2 – Outstanding Debt

The publication reveals Scottish LA debt for 2000-2001 amounts

to £9.9 billion. These figures are broken down into their constituent

parts for the general fund, trading services and the housing revenue

account as follows;

General fund services are those services financed principally

from non-domestic rates, council tax and revenue support grant

and include education, social work, roads and transport, law,

order and protective services and cleansing. The figures for 2000-2001

show that total relevant debt of all Scottish LAs amounted to

£6.3 billion and for non-relevant debt the figure was £0.5 billion.

- Trading Services & Housing RA

The costs of servicing debt on local authority

Trading Services are met mainly through the charges made for these

services, whilst the costs of servicing Housing Revenue Account

(HRA) debt are met principally from income from rents and from

Housing Support Grant. The figures for Trading Services show total

Scottish Local Authority debt at £104,078, whilst Housing Revenue

Account figures show overall debt standing at £3.5 billion for

2000-2001.

Section 3 – Local Taxes

Local taxes are an important element of financing for local authorities

accounting for a quarter of all Scottish Local Authority revenue

income. There are essentially two different types of tax levied

by local authorities, domestic taxes (council tax) and non-domestic

taxes (non-domestic rates — NDR). The publication shows that

at April 2001 the total non-domestic rateable value of all Scotland's

local authorities stood at £4.3 billion. In addition, Scottish

Local Authorities income from non-domestic rates stood at £1.6

billion and income from Council Tax stood at £1.6 billion also.

Information for branches

Be aware that the publication provides a useful breakdown of

Scottish LA spending on services including employee costs. For

example out of a total expenditure on Law, Order & Protective

Services of £1.04 billion employee costs stood at £920 million.

Of this £736million was spent on Police and £182 on the Fire Services.

Contacts list:

Dave Watson - d.watson@unison.co.uk

@ The P&I Team

14 West Campbell St

Glasgow G26RX

Tel 0845 355 0845

Fax 0141-307 2572

|